What Determines the Value of My Company?

An Overview of the Valuation Process and the Sources of Value in Private Businesses, Partnerships, and Professional Practice

Introduction

Knowing what creates value and what your firm is worth is essential to making wealth‐creating decisions. These decisions relate to everything from investing decisions and financing choices to distribution polices and appropriate prices in control transactions and estate planning. This paper is intended to be a primer on the conceptual foundations of how value is measured and what can increase or decrease the value of your firm. For some, the expectation is that valuation is a science or a precise process. For others, the view is that valuation is art where appraisers manipulate numbers to arrive at pre‐determined values. The truth of the matter is that the valuation process is both art and science – meant to be effected while resisting the lingering temptation to manipulate valuation outcomes.

It is helpful to view the firm from many perspectives to gain a greater understanding of value. This is especially true for owner/managers who often find it very difficult to accept that a potential buyer have a justifiably different opinion on value of the firm without being overly pessimistic regarding its prospects. With this in mind we start the discussion by building a framework of the valuation process from the perspective that the firm is nothing more that a nexus of contracts.

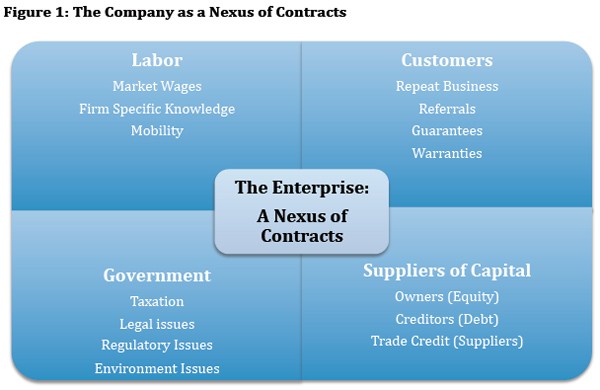

The Firm as a Nexus of Contracts

The value of the firm is the central focus of all of its stakeholders, not just the shareholders. When addressing the question of value, it is important to consider the non‐shareholder’s interests because the firm is at its core, a nexus of contracts. As such, the business owner needs to be aware of the potential impact of these other claims on the value of his or her business. Furthermore, this “contracts perspective” properly aligns the expectations of the owner who is a residual claimant. That is, the owner gets whatever remains of the accounting profits after all the other claims have been satisfied. Or in the case of a sale of the business, the owner gets whatever is left of the proceeds of the sale after all the other claims are satisfied. Nowhere is the sting of the residual claim felt more strongly than in bankruptcy, where owners typically walk away empty handed because there is nothing left for the residual claimant. Incidentally, the bankruptcy process is often described as a re‐contracting process.

Generally, the firm is contracting with four broad groups: labor, customers, government and the suppliers of capital. Each group has a unique relationship with the firm; therefore each negotiates and contracts with the firm to address the concerns and expectations that are important to it. It is these contracts, and the nature and characteristics of the groups contracting, which determine their added value to the firm. The contracts or characteristics may also result in value diminution – especially for a new owner following a control transaction. These contracting relationships are summarized in Figure 1 below.

For example, labor contracts may create relatively stable wages with predictable increases, which are often desirable characteristics for the manager of a company or for a potential investor. However, if the contracts lack the flexibility for the new owner to respond to labor market dynamics, then they may reduce the value of an enterprise saddled with potentially unsustainable labor costs. Another consideration related to the value of labor contracts relates to the ability for these contracts to induce and facilitate employee “investment in the firm.” That is, the owner of the firm prefers labor to investment its time and energy into developing firm‐specific knowledge and skills, presumably to make the company more efficient and profitable.

Likewise, an owner will also prefer employees to develop relationships with other stakeholders, such as suppliers and customers, which are value‐creative for the enterprise. Finally, the question of labor mobility must be considered. A potential purchaser of your business will want to try to determine how mobile your labor is, and how likely it is to move if there is a control transfer. These are just some of the labor related issues that a potential buyer will consider when estimating the value of your enterprise. Hand‐shake agreements, implicit understandings, and trust between you and your employees that has been nurtured over many years may have great value to you as the current owner, but less value or little value to your buyer in a control transaction because of the uncertainty related to retention.

Similarly, you and your enterprise most likely have implicit agreements and relationships and explicit contracts with your customers. Your implicit contracts and relationships may produce repeat business and referrals for your enterprise, while your explicit contracts are likely to contain guarantees and warranties on your products and services. Presumably you have developed these relationships and put these agreements and contracts in place to create value. However, a potential buyer may see less value in the agreements and may actually view the contracts in place as constraints or even liabilities, rather than assets. Taken together, the contracts in place with labor, suppliers and customers may have very different value for a prospective buyer than they have for you.

Another “partnership” that requires a great deal of attention and care is your partnership with the government. It may be unusual to think of federal, state, and local governments as your partners, but they are – they consistently take pieces of your profits through taxation. Governments also place legal, regulatory and environmental constraints on your company. These constraints may create potential liabilities for the prospective buyer, especially when the regulatory standards themselves, or the degree of enforcement of those standards, continually change. There are also times when these constraints may actually be beneficial to a business. For example, regulation may create barriers to entry for potential competitors, thereby creating a protected environment in which your firm can operate. However, the profit potential in these industries (e.g. utilities) is often restricted by the same regulations that create the favorable competitive environment.

Finally, a potential investor will consider your financing choices and how they might promote or diminish value. For example, is the firm locked into high cost debt? The cost of debt isn’t the only consideration. Because the firm obtains debt financing voluntarily, it assumes all of the constraints contained in the debt contract(s). These constraints, or covenants, may reduce the financing flexibility of the firm in the future. Furthermore, the covenants may make what is otherwise attractive assumable debt less attractive and thus reduce the value obtainable in a control transaction. The amount of debt may also be a concern. Overleveraged firms tend to be growth‐constrained, they tend to be riskier investments so new investors will seek discounted share prices, and too much leverage is often an indication of future dilution. That is, because the only financing option left for over‐leveraged firms is more equity, the new equity financing will dilute existing shareholders. Potential problems for investors may also take the form of outstanding options and warrants, dual‐class capital structures, and preferred shares. The existence of these securities raise issues related to dilution and control, voting rights and control, and distribution preference, respectively. In sum, the existing contracts of the firm may allow a seller to transfer more value to a buyer and thus receive a higher selling price all else equal. Alternatively, existing contracts, and potential legal, regulatory, or environmental issues may greatly reduce the value a seller may receive in a control transaction.

Foundations of Value, the Valuation Process & Wealth Creation

The valuation process is full of potential pitfalls and problems. It requires one to determine the purpose of the valuation that will initially create the proper framework for the valuation process and related outcomes. In general, the process requires the definition of value, the proper perspective to set guidelines and expectations, the quantification of expectations, and some refinement before arriving at a reasonable estimate of value for your firm.

Intrinsic Value is Unobservable

Any discussion about value requires the definition of value. This may sound elementary but in reality we have book values, market values, present values, option values, replacement values, and liquidation values. We also have specific guidelines given by the IRS to determine something called “fair value”.1

Therefore, when we are discussing value we need to know exactly what it is we are considering (e.g. a single tangible or intangible asset, a liability, a firm, an option) and the purpose of the valuation (e.g. going‐concern, buy/sell transaction, estate tax planning, liquidation, etc.). When it comes to valuing a firm, what we are really attempting to do is determine its intrinsic value. That is, intrinsic value is a value that everyone would agree on if we all had the same set of information and expectations about the firm. Obviously, this isn’t the case, so the job of an appraiser is to estimate the value of your company. To do that, the appraiser needs to take an objective look at your enterprise.

It is also useful to note here that the existence of intangible assets makes the job of enterprise appraisal much more difficult and increases the likelihood that the perception of value can differ dramatically between the seller and the buyer, or between the owner and the IRS. Therefore, owners of companies whose assets are largely intangible may find it particularly difficult to determine the value of the companies with a great degree of certainty. That is, any valuation estimate produced for such a firm is likely to be bounded by very wide ranges of value.

Thinking like an Investor

When considering the value of an enterprise, and asset, or a liability, one should focus on the size of the related future cash flows, the timing of those future cash flows, and the uncertainty associated with those cash flows. The risk helps investors determine appropriate expected returns from investment.

Rational investors engage in investments that are expected to create wealth. Wealth is created when realized returns exceed expected returns. This basic concept is fundamental to successful investing. So, what does this mean for the value of your firm? It means that in order to understand a potential buyer’s perspective you need consider the buyer’s returns expectations. You may be perfectly content to earn a 10% percent return on your equity capital, but other investors in the industry, or related industries, may consider a 10% return insufficient for the level of risk in your business. Therefore, for investment purposes they will expect higher rates of return. In order to have a realistic chance at earning those higher returns the potential buyers or investors will place a lower value on your business than you do. Investors want to be paid for the risk they are taking. You should too. All else equal, higher perceived risk results in higher expected returns, which in turn, result in lower valuations.2

It is also important to realize that there are value drivers that are common to almost every firm. These value drivers include the growth rate in revenues and earnings, return on assets, return on invested capital, and most particularly return on equity. If your firm is able to consistently produce relatively high rates for most or all of these variables you already know that your firm is creating wealth for you and that you can and should expect relatively high offer prices if you ever decide to sell. Alternatively, if your firm is producing at modest or poor rates, expect modest or poor prices and fewer offers.

Embrace Estimation and Forecasting

Recall that when we are thinking like investors we are considering the size, timing, and uncertainty of future cash flows. Because every acceptable valuation method relies on expectations of the future, they are necessarily dependent on estimation and forecasting. But which valuation methods and estimators should we consider?

The following list contains those that are frequently used:

- Book value of equity (accounting estimate of value)

- Market value per share (market estimate of value)

- Discounted cash flows (theoretical estimate of value)

- Option values (theoretical estimate of value)

- Replacement values (market estimate of value of similar assets)

- Liquidation values (market‐based estimate of value of similar assets)

- Guideline company multiples (market estimate of value of similar firms)

- Guideline transactions multiples (acquirer’s estimate of value of similar firms)

At this point it’s natural to stop and ask: Why are there so many different methods and estimators? The answer is straight‐forward – each method or estimator has strengths and weaknesses. Each can be rationally applied to the valuation process but each is subject to biases. Therefore, when an appraiser goes through the valuation processes he or she should provide at least two or three valuation methods to the exercise and triangulate a value range (e.g. for negotiations) or a specific value (e.g. for estate tax purposes) for your company. This brings us to the valuation process itself.

It’s all about the Process

An acceptable valuation is defined by adherence to the rules of the valuation methods employed, and not by some desired outcome. The process requires that the appraiser apply judgment and careful attention through out the valuation exercise. Careful attention to the mechanical processes of valuation methodologies alone is likely to render a less useful value. Even worse, if one quickly and thoughtlessly inserts accounting data a valuation model without much thought, the best one can hope for is a useless value. It is more likely that this approach will render an inaccurate and misleading value. Ultimately, a reasonable valuation is obtained from the application of knowledge, experience and wisdom to the data gathered, estimated, and included in the valuation model or methodology.

It is also noteworthy to understand that business appraisers are typically not industry specialists, but rather valuation specialists. While some appraisers specialize in certain industries (e.g. real estate), it is more common for an appraiser to rely on business owners for the industry specific knowledge necessary to complete a valuation analysis. This isn’t to say that generalists won’t have other resources to use in analyzing your firm and the related industry. They do. However, because each industry operates in unique ways, your knowledge and experience will allow a generalist to capture all the essential nuances related to the value of your firm. As firm size increases and business activities become more complex, it makes sense for owners to consider using more expensive industry specialists. At this level the specialist may have access to data, knowledge, or an understanding of the industry that you haven’t yet acquired. He or she can bring these into the valuation analysis to make it more complete. However, for most privately held firms the trade‐off between cost and additional insights isn’t justified. The lower cost generalist will be able to provide an accurate estimate of value with your firm.

Think Critically

Once the base case assumptions have been determined, they have to be tested. That is, the valuation process should include scenario testing and sensitivity testing to scrutinize the assumptions used therein. In reality, it is easy to select variable values in isolation, only to learn later that the variables and their associated values interact in unexpected ways. Thus, the valuation process is an iterative one, requiring feedback and refinement. Ultimately, the valuation process requires critical thinking about the inputs and the outputs to ensure the integrity of the process and the reasonableness of the valuation outcomes.

Some Other Considerations

Other considerations beyond the contracts perspective, value drivers and the valuation process include the application of premiums and discounts, and identifying pitfalls in the valuation process. These are addressed briefly below.

Control Premiums and Related Discounts

In addition to valuing your firm as a going concern, some other firm characteristics may require adjustments to that value. For example, if there is a control position (e.g. a single investor can determine or influence the outcome of major company decisions, or in many cases, all of the companies decisions), then any other shareholders are necessarily in minority positions. Minority positions are less valuable than control positions and are therefore subject to discounts. There are also discounts for lack of marketability (think private firms where no market for its shares exists) and discounts for the lack of liquidity (e.g. shares that are contractually prohibited from sale for any period of time). These adjustments to value can have a profound effect on the value of shares in private companies and the value of minority shares.

What Valuation is Not

It is tempting for owners to find quick and inexpensive ways to estimate the values of their companies. For example, an owner may have an accountant or another trusted professional advise them on the going rate for firms like their own. The advice may take a form such as “just use one times revenues to find the value of your company” or some other rule of thumb. This approach, while inexpensive and easy to use and understand, has little hope of helping an owner arrive at a fair or reasonable value for his or her company. Moreover, the IRS will not accept valued derived such methodologies. In addition to the value drivers already mentioned, firm characteristics such as expected growth rates, profit margins, distribution policies, capital structure, off‐balance sheet financing, the ratio of tangible assets to total assets, and the cost and availability of capital might cause the value of firms to vary dramatically. There is little chance that your firm is sufficiently similar to another firm that just sold that you would want to use that firm’s valuation multiples without some serious comparisons and analysis.

It is also tempting to borrow valuation multiples (e.g. price‐earnings multiples) from publicly traded firms and apply them to your own firm to arrive at a fair value. This method is also incorrect for the previously mentioned reasons. In addition, the powerful influences of control premiums, minority discounts, and other discounts may create additional material biases in the resulting value.

Finally, as mentioned previously, the valuation process is not intended to arrive at some pre‐determined value through manipulation of the methods and estimators that are employed. Rather, the process is intended to guide an appraiser through the application of valuation theory, reasonable estimators and assumptions, and judgment and experience in order to arrive at a reasonable and credible valuation outcome.

Summary

The valuation process is complex and requires the tools of valuation theory as well as the judgment, knowledge, and skill possessed by an experienced appraiser. As a business owner, there are many things you can do to add value to your firm, and create wealth for yourself and your family. Ultimately, whatever those actions are, they need to facilitate relatively high and sustainable growth in revenues and earnings, while minimizing the amount of invested capital. The resulting high returns on invested capital and even higher returns to equity will make your company more valuable and more attractive to any potential buyer.

1 A widely accepted standard for valuing a closely held business is fair market value as defined by Treasury Regulations ¤25.5212‐1. All federal and state tax matters (estate taxes, gift taxes, income taxes, etc.) require the standard of fair market value. Revenue Ruling 59‐60 defines fair market value as: …the price at which the property would change hands between a willing buyer and a willing seller when the former is not under any compulsion to buy and the latter is not under any compulsion to sell, both parties having a reasonable knowledge of relevant facts. Court decisions frequently state in addition that the hypothetical buyer and seller are assumed to be able, as well as willing, to trade and be well informed about the property and concerning the market for such property.

2 A simple example illustrates this point. Consider an investor facing an investment opportunity that costs $1,000 and has an expected payoff of $1,100. Such an opportunity is offering a 10% return. If the investor is satisfied with this expected return then he or she will comfortably and willingly invest $1,000. However, if the investor was expecting a higher rate of return, say 15%, then he or she would be willing to invest no more than $956.52. At this price the expected return one the same investment opportunity is 15%.

Reverences

- Bruner, Robert F, Applied Mergers and Acquisitions, 3rd ed., John Wiley & Sons, 2004.

- Damodaran, Aswath, Damodaran on Valuation, 2nd ed., John Wiley & Sons, 2006.

- Koller, Tim, Marc Goedhart and David Wessels, Valuation: Measuring and Managing the Value of Companies, 5th ed., John Wiley & Sons, 2010.

- Goedhart, Marc, Timothy Koller and David Wessels, The Right Role for Multiples in Valuation, McKinsey on Finance, Number 15, Spring 2005.

© 2010 The Center for Valuation Studies | www.valuationstudies.com

We serve the estate planning needs of individuals, families and business owners.

We take time to understand and plan for your goals, your values, and your uniqueness.